말레이시아 전화 012 722 2308

한국 인터넷전화 070 8800 4875

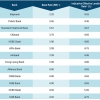

최근 말레이시아 대출 이자 산정 방식이 BLR 마이너스 적용에서 BR 플러스 방식으로 변경되었습니다.

Planning to apply for a loan this year? Here's what you need to know first: Base Rate vs BLR in Malaysia: How Does BR Work?

Effective January 2, 2015, the Base Lending Rate (BLR) structure was replaced with a new Base Rate (BR) system. Under BR, which will now serve as the main reference rate for new retail floating rate loans, banks in Malaysia can determine their interest rate based on a formula set by the central bank.

Under the previous BLR, the rate was set by Bank Negara Malaysia (BNM) based on how much it costs to lend money to other financial institutions. Meanwhile, the cost to borrow money was determined by the Overnight Policy Rate (OPR) set by central bank.

With the new BR, interest rates are determined by the banks’ benchmark cost of funds and Statutory Reserve Requirement (SRR). Other components of loan pricing such as borrower credit risk, liquidity risk premium, operating costs and profit margin will be reflected in a spread in the new BR framework.

Why the change?

Instead of a fixed rate under BLR, BR are determined by banks without intervention by the central bank, and should differ from bank to bank depending on their own efficiencies in lending. Banks with a strong niche in consumer financing such as Maybank and Public Bank will have the initial edge of being able to offer more attractive and competitive BR and effective lending rates (ELR) for their customers.

The new framework encourages greater transparency from banks and will enable customers to make better financial decisions. Previously, calculations of BLR lacked transparency and some banks were lending below the BLR to attract customers and boost loan growth. Under the new system, customers cannot borrow below the base rate.

How does it affect you?

The change towards the new framework should have minimum impact on borrowers. Take the rates offered by Maybank for example. Based on the previous BLR rate of 6.85%, the “BLR -2.40%” offer means that the customer pays 4.45% on the mortgage.

With the BR system, the bank will have to reveal its base rate and also disclose its margin, which will determine the ELR. Maybank has set its Base Rate (BR) at 3.20%. Here, interest is presented as “base rate +1.35%”, which means that the effective rate that the customer will have to pay on the mortgage is 4.55%.

Ultimately, it’s the ELR that will determine how much you will have to pay for your mortgage. Here is a comparison of how much you will be paying for your home loan under BLR and under BR.

Though certain banks may be setting a higher BR compared to others, they can sometimes offer lower ELR to customers in order to remain competitive. For example, Public Bank has a BR of 3.65% while Maybank’s is 3.20%. However, Public Bank offers a lower ELR at 4.45%, while Maybank’s ELR is 4.55%. This essentially means that Public Bank is willing to take a smaller profit margin in order to be more competitive.

Loans that are already approved and extended prior to January 2, 2015 will still follow the old BLR until the end of the loan tenure.

For new loan applicants and refinancing applicants, the new BR framework will have a direct impact on interest rates with effect from the date. Banks are still required to display both BLR and BR on their branches and websites.

What happens now?

Better transparency will create healthy competition among banks and provide a wider range of options for loan applicants. According to BNM, the new reference rate will also better reflect changes in cost arising from monetary policy and market funding conditions, while encouraging greater discipline and efficiency among financial institutions in the pricing of retail financing products.

Also, because the base rates are managed by individual banks, this will force banks to come up with more cost-efficient rates in order to compete with each other and create a much more competitive market.

However, given the flexibility to determine their respective benchmark rates, smaller institutions may risk losing out on the race of getting more borrowers for loans.

Bigger establishments will have more room to maneuver when determining the reference rates, whereas smaller institutions may not have as much leeway to offer competitive rates. However, loan rates will still depend on the management’s risk appetite at the end of the day.

For the customer, a more transparent reference rate will enable them to make better money choices when it comes to navigating an array of loan products offered by various financial institutions. Customers with a higher risk profile such as those with bad credit, low income or poor employment histories will enable the bank to set the ELR higher and make a more profitable net interest margin (NIM). However, this could result in potentially higher default rates in the future.

Home buyers can keep ahead with the rates (new and old) by comparing all the best home loan rates from the banks before making a decision on which loan to apply for. By doing thorough and adequate research, you can remove some of the intimidation factor from the home-buying process.

Text: Fiona Ho, iMoney

Image: iMoney

Andy Ko, DH 고동한

REAPFIELD PROPERTIES(HARTAMAS) SDN BHD

HP : +60 (0)12-722 2308 Malaysia

OFFICE : +60 (0)3-2300 1813

FAX : +60 (0)3-2300 1823

EMAIL: andyko@reapfield.com

부동산 매물 리스트 : http://malaymyhome.com/

한국 연락처 : 070-8800-4875 핸드폰 011-613-1967

| 번호 | 제목 | 닉네임 | 조회 | 등록일 | |

|---|---|---|---|---|---|

| 6 |

|

몽키아라 부동산 투어 일정 공지

|

|||

andyko |

31360 | 2015-11-23 | |||

|

립필드에서 몽키아라 부동산 투어를 합니다. 투자 장점과 향후 개발계획, KL메트로폴리스와 연계된 부동산 동향에 대해 자세히 설명 들으실 수 있습니다. 투어에 관심있으신 분께서는 연락주시면 참석할 수 있도록 일정 잡아 드립니다. 감...

|

|||||

|

|

말레이시아 부동산 구입시 대출 이자 및 비용

|

|||

andyko |

26564 | 2015-02-23 | |||

|

최근 말레이시아 대출 이자 산정 방식이 BLR 마이너스 적용에서 BR 플러스 방식으로 변경되었습니다. Planning to apply for a loan this year? Here's what you need to know first: Base Rate vs BLR in Malaysia: How Do...

|

|||||

| 4 |

|

키아라빌 1600sf 임대유닛 풀퍼니쳐

|

|||

andyko |

24937 | 2013-09-05 | |||

|

키아라빌 임대물건 1600sf, 방3개, 풀퍼니쳐, 고층 유닛

|

|||||

| 3 |

|

KL시내 중심가의 프로젝트 분양 안내 - FACE

|

|||

andyko |

12485 | 2013-07-21 | |||

|

안녕하세요? 한국에 다녀오느라 정작 말레이시아 계신분들께는 그동안의 매물을 소개해 드리지 못했네요 ^^; 아래 분양건은 저희 Reapfield 에서 진행하는 프로젝트 입니다. 매입 전과정에 대하여 안전하고 투명하게 진행해 드립니다. KL시...

|

|||||

| 2 |

|

아유리아 다양한 유닛 임대물건 있습니다.

|

|||

andyko |

26635 | 2013-03-29 | |||

|

안녕하세요? 수영장이 좋아서 아이들에게 인기가 있는 아유리아 콘도 다양한 유닛 임대 물건입니다. 대부분 풀퍼니쳐로 임대하고 있으나 파틀리 퍼니쉬도 가능합니다. 아래 사진은 모두 실제 임대매물의 사진입니다. 물론 입주시에 깨끗하게...

|

|||||

| 1 |

|

암팡 푸트라 매도 / 임대 유닛

|

|||

andyko |

11574 | 2012-09-18 | |||

|

안녕하세요?

암팡푸트라 매도 물건입니다.

리노베이션 되어있고 가전가구 포함하여 매도합니다.

사이즈는 약 1500sf, 매도가격은 660,000링깃입니다.

풀퍼니쳐 임대가격 3,300링깃

은행대출신청 및 변호사 서류진행 일괄진행하여 드립니다...

|

|||||